7 things Texas families need to know for school choice 2026/27

How the sweeping, federal budget-reconciliation package (OBBB) and Texas state policies impact your school choice options next year.

Cecilia Retelle Zywicki

CEO, LearningSpring

Introduction

In July 2025, Congress passed a sweeping budget-reconciliation package often referred to as the One Big Beautiful Bill (also called H.R. 1 or the Working Families Tax Cuts Act, WFTCA for short). Among many fiscal and tax changes, the law includes a new federal tax credit scholarship program under Section 70411. That federal mechanism creates incentives for states to adopt or expand school choice programs, but it doesn't itself directly send money to families. From there, each state (including Texas) must make decisions about how to structure its own programs.

Here are eight key things for Texas parents and families to understand as you plan ahead for 2026-27:

1. The new federal incentive for Scholarship Granting Organizations (SGOs)

Section 70411 of WFTCA establishes a new federal tax credit that allows individuals to receive a nonrefundable dollar-for-dollar reduction in federal taxes for contributions to qualified Scholarship Granting Organizations (SGOs) in states that adopt the program.

The credit is capped (for individuals) at $1,700 per year (with potentially different limits for married filers) for cash donations to those SGOs.

Scholarships distributed by SGOs are excluded from the recipient's gross income for federal tax purposes.

States must opt in. The federal credit doesn't automatically apply everywhere. The program is designed so that states decide whether to certify SGOs and allow students in their jurisdiction to benefit.

The effective start for tax years is after December 31, 2026. So scholarships and credits under this program would begin in tax year 2027.

In short: Section 70411 is a federal “push” — it creates a tax incentive for donors to invest in school scholarships, but the actual flow of scholarship funds is mediated by state law.

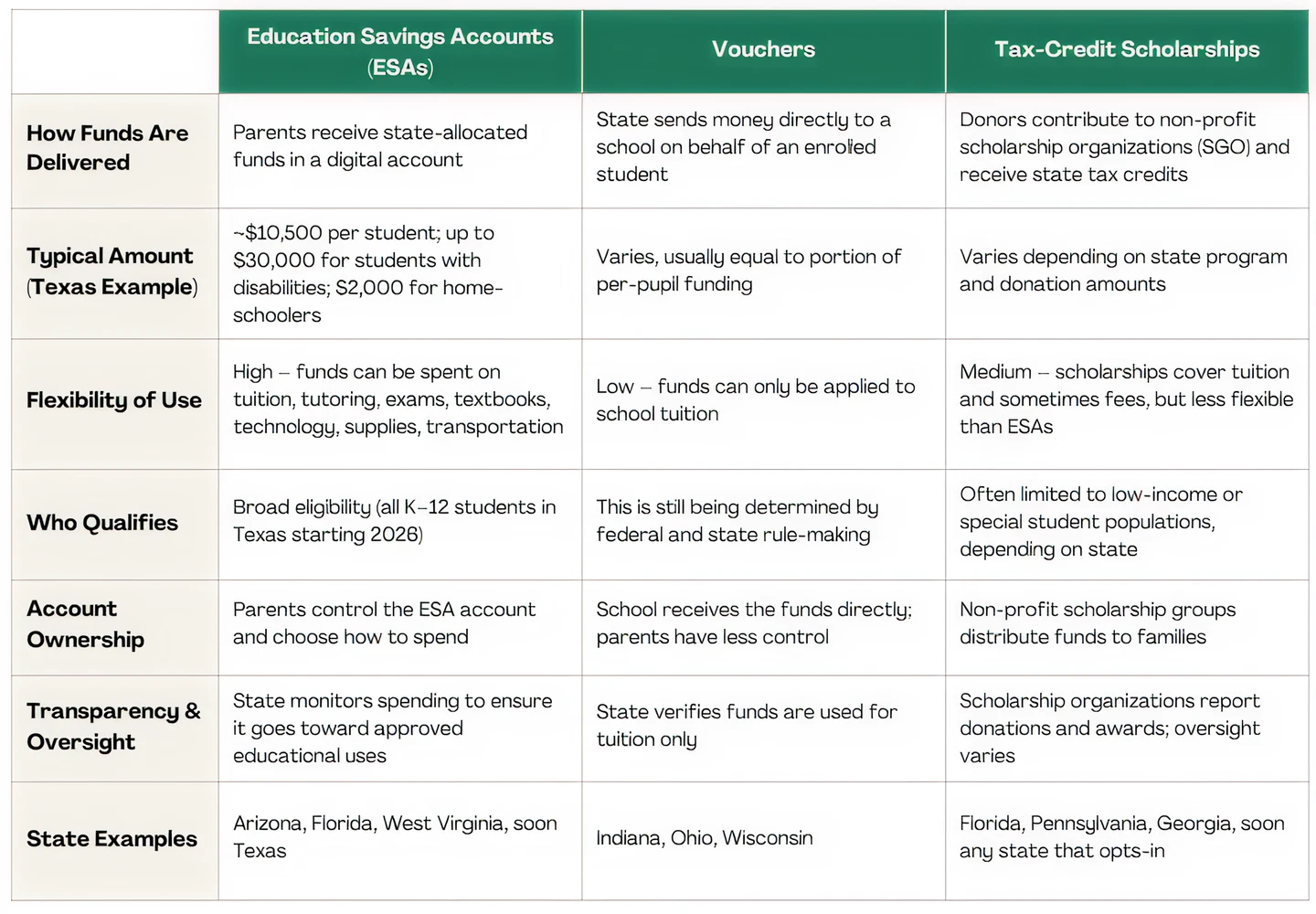

2. The federal credit is not a direct voucher or ESA at the national level

It's easy to conflate this with vouchers or education savings accounts (ESAs), but the Section 70411 framework differs:

The federal law does not require or mandate that states provide direct-to-family grants, ESAs, or vouchers. It creates infrastructure for privately funded scholarships.

Families cannot simply “opt in” to get federal money; they benefit only if their state establishes an SGO program and participates.

The donation side of the program is what is federally incentivized (through the tax credit), rather than government depositing funds into a child's account.

In essence, the federal law establishes a public-private funding mechanism to expand school choice—but leaves the structure and rules up to states.

3. State choice is a key decision point

Texas must enact or adapt a state-level scholarship/choice mechanism that aligns with the federal framework to unlock the benefits for its residents. Some states may choose to certify SGOs, others may combine this with existing voucher or ESA programs, or may layer rules of eligibility (income, disability, etc.).

Because the federal credit kicks in only if states adopt compatible systems, the timing, rules, and design in Texas will matter greatly for how families can take advantage.

5. The federal credit could expand private funding

One of Section 70411's goals is to encourage private philanthropy for K-12 scholarships:

Donors would get a federal tax benefit to contribute to SGOs

Texas families might see more scholarship dollars available beyond what the state itself budgets

6. Tradeoffs, gains, and risks

As with any major reform, there are potential benefits and risks:

Speed & Rollout Administration: The rapid increase in scholarship and giving mechanisms with little resources or time to prepare may leave families feeling lost or confused of how to use their school choice options

Equity & Access: How Texas designs eligibility (e.g. income caps, disability priority) will influence whether low-income families benefit.

Accountability & Transparency: Scholarship programs must include safeguards to ensure quality and prevent misuse.

Timing Gaps: Federal incentives begin in 2027; states and scholarship organizations must build infrastructure before then.

7. What Texas families should do to prepare

Here's how to get ahead:

Follow state legislation: Monitor bills in the Texas Legislature that adopt or refine ESA, voucher, or SGO frameworks. Texas is expected to opt-in to the federal program.

Engage local advocacy groups: Many parent and school-choice groups will push for favorable rules—get involved early.

Research options: Sign up for a LearningSpring account to understand what schools and services you might want (public school, private school, tutoring, therapy, etc.) in you area.

Watch certification rules: For an SGO to be valid, the state must certify it under the federal law.

Time your application: The first rounds of scholarship eligibility may lag behind the federal law's effective date (2027). Families may be invited in phases starting with low-income or disabled students.

Plan philanthropically: In the longer run, some families or community donors may use the federal credit to support scholarship programs.

Bottom line

The new federal legislation in the OBBB or WFTCA sets up a federal tax credit scholarship program, but it does not itself create a universal voucher or ESA at the federal level. The power lies with states to opt in and design compatible systems. For Texas families, the key is watching how state lawmakers adopt and implement SGO or ESA policies in a way that lets you use federal incentives and expand school choice in 2026–27 and beyond.

Share this post

Create a Free LearningSpring Parent Account

Search and save schools to your favorites. Make notes and come back later. It’s a big decision -- let LearningSpring be a helpful school choice toolset.